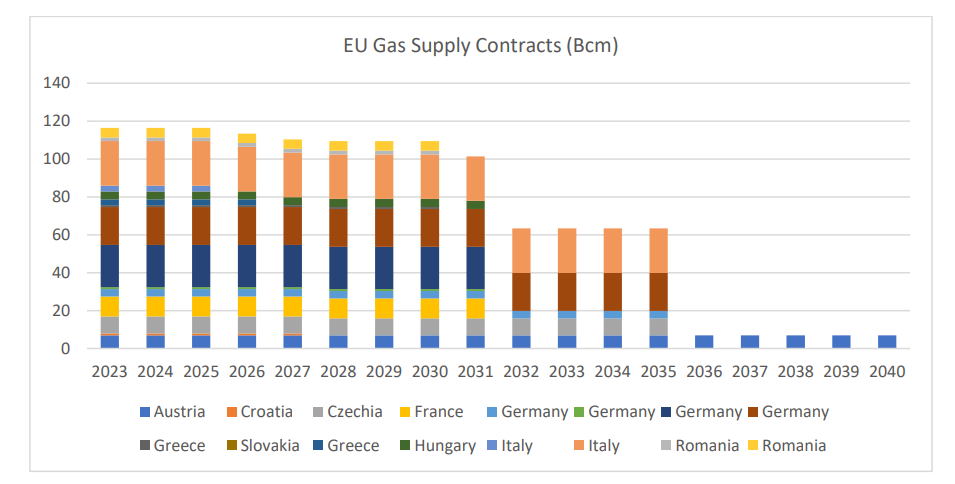

it is estimated that at least 116.4 Bcm/year of annual contracted quantities via gas pipeline are still contracted between EU countries and Gazprom or one of its subsidiaries. What’s the likely outcome for these dormant contracts? If some Russian contracts were to remain in place, they could cushion the impact of LNG price volatility… This contracted volume is way above current […]

ADVERTISEMENT